Personal Tax Rates

The Government will deliver more tax cuts to all Australian taxpayers, with additional tax cuts in 2026 and 2027.

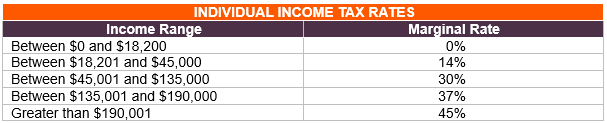

- From 1 July 2026, the 16 per cent tax rate, which applies to taxable income between $18,201-$45,000 will reduce to 15%.

- From July 2027 this rate will be reduced further to 14 per cent.

The tax saving from the tax cuts represents a maximum of $268 in the year 2026/2027 and $536 from the 2027/2028 year.

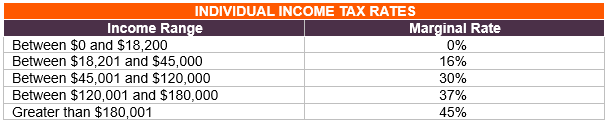

Current Tax Rates (20-24/25)

Redesigned Tax Rates – From 1 July 2026

Redesigned Tax Rates – From 1 July 2027

Medicare Levy Changes

The Government will also increase the Medicare levy low-income threshold by 4.7% for singles, families and seniors and pensioners from 1 July 2024. This change will mean over one million Australians on lower incomes will continue to be exempt from paying the Medicare Levy of pay a reduced levy rate.

Childcare Subsidy

The Government has announced from 1 January 2026 the current activity test will be removed and three days of subsidised childcare for families with young children will be available regardless of how much they work or study. The subsidy will remain income tested.

Non Compete Clauses To Be Banned

From 2027 the Government has announced that it will ban non-compete clauses for low and middle-income employees (currently considered to be those earning less than $175,000). These clauses in employment contracts prevent or restrict employees from moving to a competitor and the removal of these clauses will allow employees to start their own business or move to alternative employment.

Two-year Ban On Foreign Ownership Of Established Homes

As announced on 16 February 2025, foreign persons will be banned from purchasing established dwellings in Australia for at least two years. This measure means that foreign persons, including temporary residents and foreign-owned companies, cannot apply to buy an established dwelling in Australia unless an exception applies (such as providing housing for workers under the Pacific Australia Labour Mobility (PALM) scheme). The ban does not apply to permanent residents, New Zealand citizens and spouses of either if buying as joint tenants.

Energy Bill Relief Fund – Extension And Expansion

To help ease cost-of-living pressures, the Government has announced a new measure where eligible households and small businesses will receive a total of $150 off their energy bills. This will be provided as two quarterly rebates of $75 each, from 1 July 2025 to 31 December 2025. Like the previous energy bill relief measures, these rebates will be automatically applied to electricity bills in quarterly instalments.

Update On Measures Previously Announced

Payday Super

Starting from 1 July 2026, as outlined in the Federal Budget 2023–24, employers will be required to make superannuation payments to their employees at the same time as their salary and wages, to prevent late paid superannuation. Draft legislation and explanatory materials on this matter were recently released for consultation on 14 March 2025.

Division 296

This proposes to impose a 15% tax on earnings from the portion of an individual’s total superannuation balance that exceeds $3 million. Despite feedback given surrounding the concerns around taxing unrealised gains, the enabling bill remains unchanged, however it has not been legislated. The previous announcement had this measure commencing on 1 July 2025. Note that Budget revenues include income from this measure therefore we expect this to be a current Government position leading into the upcoming election.

Denied deduction for GIC & SIC

A proposal to disallow deductions for general interest charge (GIC) and shortfall interest charge (SIC) was introduced in the Mid-Year Economic and Fiscal Outlook 2023–24. This is now law and any GIC & SIC deductions incurred on or after 1 July 2025 are no longer deductible for all entity types.

Student Loan Reduction

The Government is looking to reduce individual’s student loans with a one-off 20% reduction. This will apply to an individual’s balance, pre indexation, on 1 June 2025. This is yet to be legislated.

Help to Buy Program Extended

This program reduces the deposit required to buy a home by providing an equity contribution by the Government. Previously, to be eligible for the program, the income threshold for an individual was $90,000 and, for joint applicants, $120,000. As announced, these thresholds will increase to $100,000 and $160,000, respectively.

$20,000 Instant Asset Write-off

The Government has reaffirmed its commitment to extend the $20,000 instant asset write-off threshold by 12 months, until 30 June 2025. This measure, initially announced in last year’s budget, was finally legislated last week. There is no announced extension of this measure for the 2025-26 financial year, therefore the threshold will reduce back down to $1,000 from 1 July 2025.