With the Australian Taxation Office (ATO) cracking down on anti-compliance, their penalties and interest charges continue to be on the stricter side. This article provides an overview of these penalties and the current interest rates.

1. Penalties for Non-Compliance

The ATO imposes administrative penalties for two key reasons:

- False or misleading statements

- Failure to lodge documents on time

A. False or Misleading Statements

Penalties may apply if a taxpayer makes a false or misleading statement. The term “false and misleading” is hazy, but taxpayers can avoid penalties if they demonstrate adequate care.

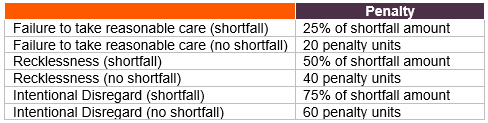

Once it can be concluded that the taxpayer has made a false or misleading statement, or they have failed to take reasonable care – the applicable penalties are calculated as follows:

Shortfall amount refers to the additional tax payable after the impact of the false or misleading statement is removed from one’s tax liability calculations.

The taxpayer may be liable for additional penalties if the taxpayer obstructs the ATO or fails to disclose errors after discovering them.

B. Failure to Lodge Documents on Time

Penalties are also applicable on failure to lodge documents, such as Income Tax Returns and Business Activity Statements on time.

Penalty amounts vary by the type of entity.

2. Interest Charges

The ATO imposes interest charges on liabilities in two primary ways:

A. Shortfall Interest Charge (SIC)

SIC applies when a document lodged with the ATO is amended and the amendment results in amounts being payable. It is the base interest rate* plus 3% and calculated on a daily basis for every day between the due date of the original lodgement and the amendment. It is not compounded.

B. General Interest Charge (GIC)

When SIC is not applicable, the GIC is applied. This generally involves amounts which have not been settled by their respective due dates.

GIC is compounded daily and stands to be the base interest rate plus 7%.

*Base interest rate is the average yield on a 90-day bank bill published by the RBA.

date.

How to avoid Penalties and Interest?

To minimize penalties and interest:

- Regularly check deadlines and obligations.

- If you anticipate issues, contact the ATO proactively

- Consult a tax advisor for guidance on compliance.