Something was definitely in the water in the offices of Harris Black earlier this year given the arrival of five new HB family members in the last few months! Such a wonderful time for us all waiting for each of these beautiful babies to arrive… It’s been a great experience of anticipation and excitement over recent months for the entire office!

Heartfelt congratulations to Harris Black team members Kim Ward, Taylor Dicken, Louise Chen, Olivia Beckett, Tomoka Kawamoto and their partners!

Baby Elijah James Ward born to Kim Ward and husband James on 28 May 2022

Baby Charlie Dicken born to Taylor Dicken and his partner Jacinta on 5 July 2022

Baby Theodore Chen born to Louise and Simon Chen on 5 August 2022

Baby Luca Weston Beckettborn to Olivia Beckett and husband Adam on 9 August 2022

Baby Maya Kawamotoborn to Tomoka and Anthony Kawamoto on 22 August 2022

Lodge Annual TFN withholding report 2022 if a trustee of a closely held trust has been acquired to withhold amounts from payments to beneficiaries.

21 October 2022

Pay annual PAYG Instalment Notice.

Lodge and pay quarter 1, 2022-23 PAYG instalment for head companies of consolidated groups.

Lodge and pay annual activity statements for TFN withholding for closely held trusts where a trustee withheld amounts from payments to beneficiaries during the 2021-22 income year.

Procrastination can often slow down the decision- making process in your business. In this video Renee Bettenay, Director from Harris Black, will discuss the 5 ways leaders tend to procrastinate and offer some solutions to help drive to quicker decision making within your business.

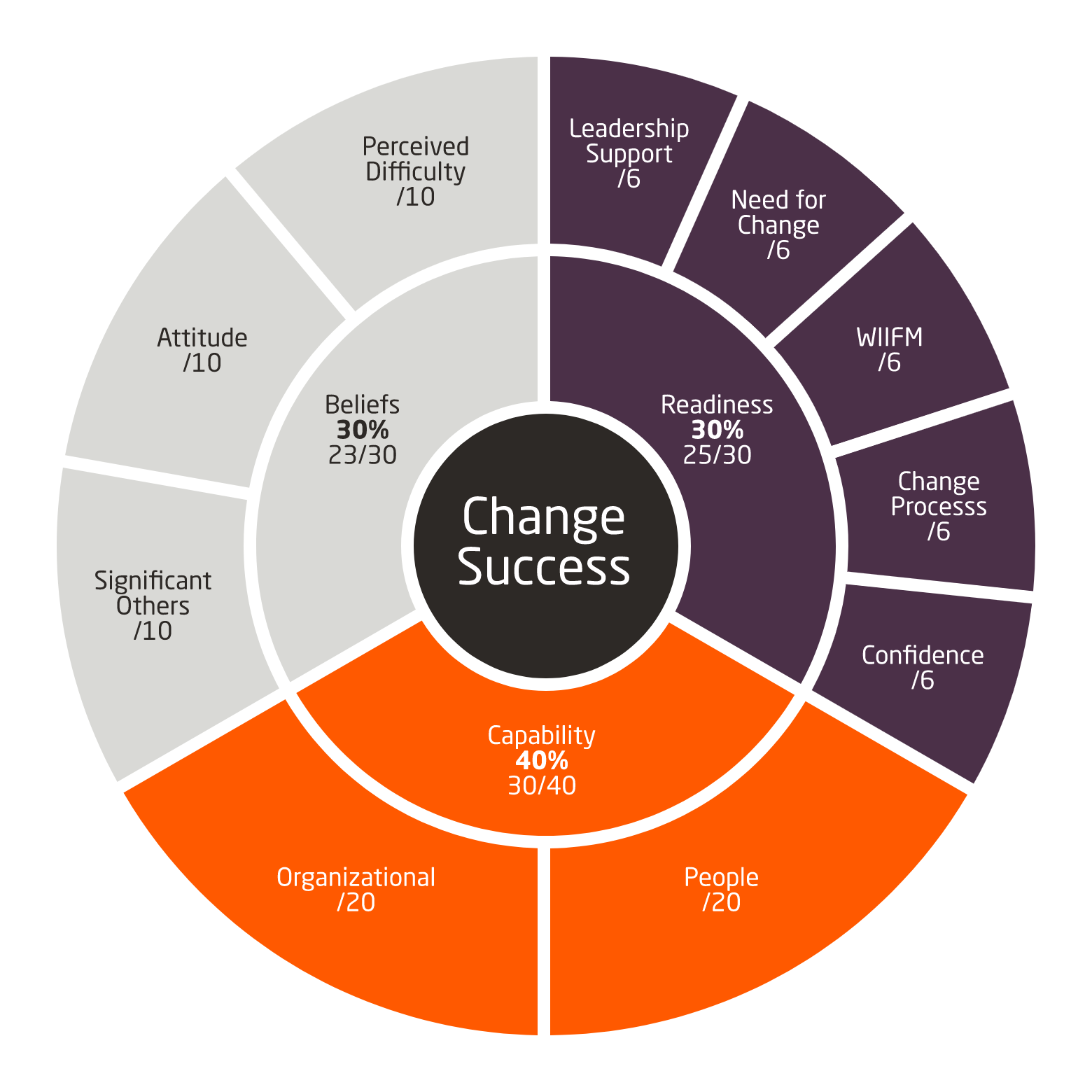

Research tells us there is only a 30% probability your change initiative will succeed. This is because most business people adopt a ‘trial and error’ approach to change incurring a high cost in terms of lost time, reduced confidence, wasted money and poor resource utilisation. You can however improve this probability of change success…

Developed by Mindshop founder, Dr Chris Mason following an 8-year PhD on the subject, the change success model will identify the following outcomes:

your change potential percentage (an ideal success score being a minimum of 78%) and

which one of the ten change success factors has the biggest gap between where you are NOW and the maximum WHERE score

This report will then help you determine and implement strategies to boost your potential for change success by lifting the scores in your largest gap areas.

Opportunities abound for most businesses in 2022 yet the unpredictable, disruptive landscape each business operates in, makes implementation of strategy challenging.

In our recent workshop for the Harris Black Business Leaders Forum, we looked at ‘Essentials to building and executing an adaptive strategy in 2022’.

In this forum, we looked at the foundations to a successful, adaptive strategy in 2022 and where you have gaps in your own plans and approaches to execution. We also looked at how you will integrate ESG factors into your plans and why.

Discussed on the day:

What’s working and what’s not with your strategy in 2022 Must have in your strategy How to integrate Environmental, Social and Governance (ESG) factors into your strategies Building your adaptive strategy

Overall a terrific day with attendees walking away with clarity on practical ways they can stress test their plans and approaches to execution for the year ahead.

For more information and to book your ticket in our next HB Business Leaders Forum on the 25 August 2022, please click the Book Ticket button below.

Microsoft Excel is the ubiquitous tool for personal record keeping favoured by all from working professionals to small-business owners which allows users to track information and maintain large databases with ease.

However, as an accounting firm, Harris Black knows it is not always just about the numbers. Despite its popularity, the hidden potential of the Excel spreadsheet continues to fly under the radar.

Below, members of the Harris Black Team have noted down some handy tips and keyboard shortcuts to make your life easier and enrich your Excel experiences!

Formatting of Numbers

Use the Format function to transform your cells to improve readability!

Conditional Formatting – This formula will highlight or find data items based on a particular criteria.

Navigating

CTRL + Arrow Key – This shortcut allows you to instantly scroll the end of a row or column or even to the end of the worksheet.

CTRL + SHIFT + Arrow Keys – include the “Shift” key to the above shortcut to select all cells in a row or column.

CTRL + A – This shortcut selects all cells in a sheet, allowing you to copy and paste from one sheet to another easily.

CTRL + Page Up/Page Down – Navigate through your Excel tabs using this formula.

Presentation

Make use of the shortcuts for a simple way to hide unnecessary rows and columns in your spreadsheet.

CTRL + 9 – Hide rows

CTRL + 0 – Hide columns

Insert Column or rows in your spreadsheet using the below shortcut.

CTRL + Shift + =

Formulas

VLOOKUP/HLOOKUP – This formula allows you to find date in a table based on a selected criteria.

VLOOKUP (lookup value, range containing the lookup value, the column number in the range containing the return value, Approximate match (TRUE) or Exact match (FALSE))

All of the above may prove useful when collating your information for tax time.

How can we help you?

Today’s financial environment demands a regular review of strategy and a focus on execution.